Pre-approval vs Prequalification

If you’re starting the home buying process, you’ll hear two terms immediately:

Pre-qualification and Pre-approval

They sound similar—but in practice, they are very different tools, especially when you’re competing in a market like San Francisco.

And in this city, that difference matters more than most people realize.

Quick Breakdown

Pre-qualification = early estimate

Pre-approval = verified buying power

One is based on what you tell a lender.

The other is based on what they can prove and verify.

In competitive markets, sellers care a lot more about the verified Pre-Approval

What is Pre-qualification?

Pre-qualification is the first step in the mortgage process.

You’ll typically provide:

Income estimate

Debt information

Savings and assets

Basic credit overview (sometimes)

From there, a lender gives you a rough idea of what you might be able to afford.

What is Pre-approval?

Pre-approval is a much deeper financial review.

At this stage, the lender actually verifies:

Income (W-2s, pay stubs)

Assets and bank statements

Credit report (hard inquiry)

Employment history

After reviewing everything, the lender issues a pre-approval letter showing how much they are willing to lend you.

Why This Matters in San Francisco

In slower markets, buyers can sometimes move forward with just a prequalification.

In San Francisco, that rarely works.

Here’s why:

1. Sellers want certainty

A preapproval shows your offer is backed by verified financing—not estimates.

That reduces risk for the seller.

2. You’re competing with multiple offers

In competitive situations, sellers are looking at:

price

contingencies

closing timeline

and buyer strength

Preapproval immediately puts you in a stronger category.

3. It signals seriousness

Even before you write an offer, a preapproval tells the seller:

“This buyer is ready to close.”

That alone can change how your offer is received.

A Simple Way to Think About It

Prequalification = “I think I can buy a home around this price”

Preapproval = “A lender has verified I can actually buy in this range”

One is directionally helpful.

The other is what gets your offer taken seriously.

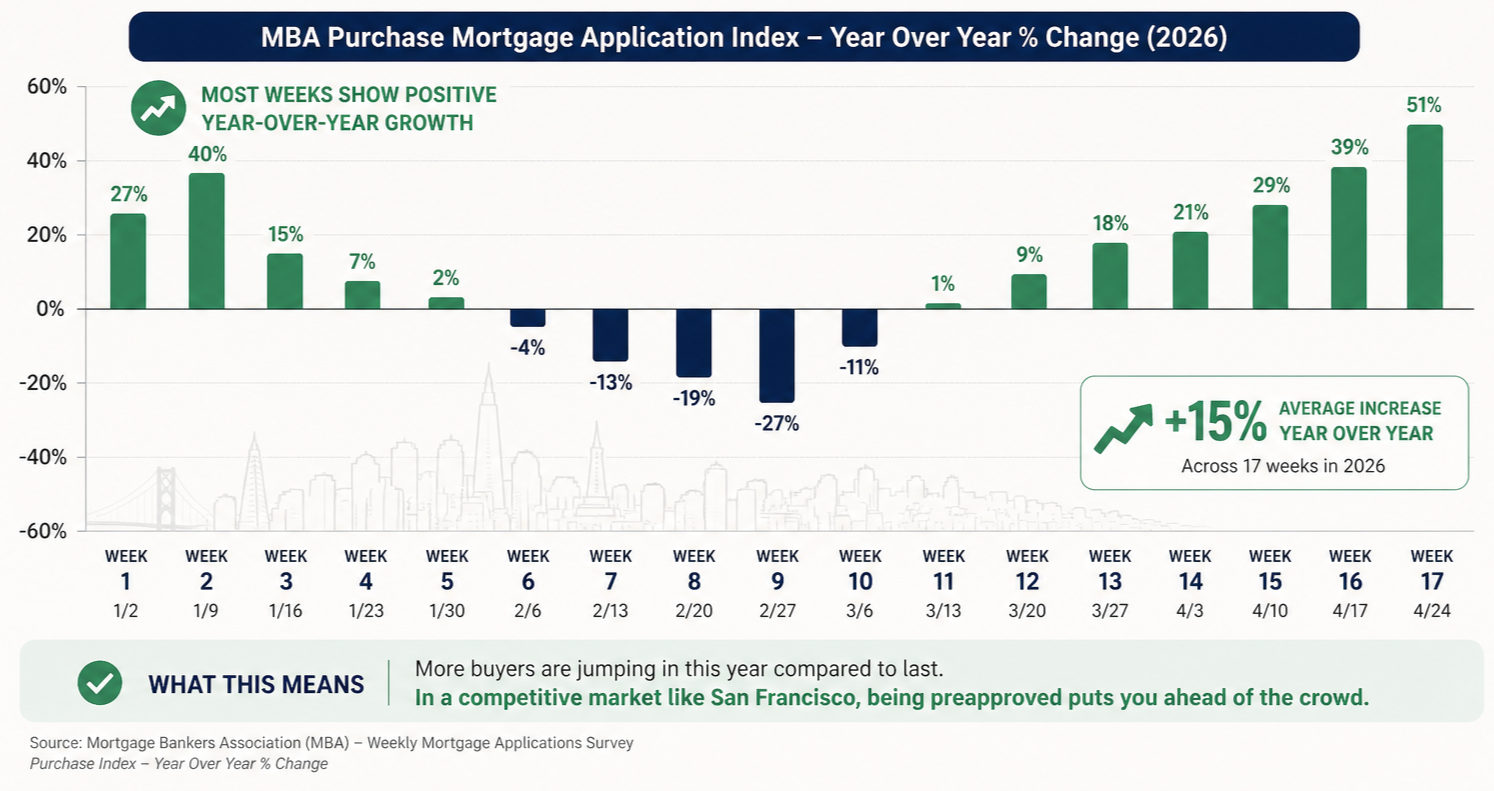

The MBA (Mortgage Bankers Association) Purchase Index —Tracking Buyer Demand

The MBA Purchase Index measures the weekly volume of new mortgage applications for home purchases. It serves as a leading indicator for the U.S. housing market; because applications precede actual sales, a rise in the index predicts an uptick in home-buying activity in the coming months.

Prequalified vs. Approved: Don’t Let Your Offer Fall Through

Before you start falling in love with listings, you need to know exactly where you stand with lenders. Many online platforms like Rocket Mortgage can be used for getting a "quick pulse" on your budget, but there is a massive difference between a 5-minute estimate and a verified commitment.

Pre-qualification: This is an informal "ballpark." It’s based on self-reported data and usually only requires a soft credit check. It's a great baseline for your own planning, but most sellers won't take an offer seriously if this is all you have.

Verified Approval: This is the "gold standard." To get this, an underwriter actually reviews your pay stubs, tax returns, and bank statements.

The Bottom Line: Use online tools for your initial research, but if you’re ready to sign a contract, make sure you have a Verified Approval Letter. In a competitive market, a "pre-qual" is just a conversation; an "approval" is a handshake.